Introduction

Picture the moment a corporate development interview turns to financials — the interviewer slides a balance sheet across the table and asks you to walk through it. Most JDs go blank. Law school trains you to read dense documents, spot inconsistencies, and construct arguments from evidence. Those are exactly the skills financial statement analysis demands, yet most lawyers enter business roles without ever having opened a balance sheet in a professional context.

ABA accreditation standards don't require accounting or finance coursework. The result: lawyers who are analytically sharp but financially underprepared hit a real wall when business interviews ask them to walk through a company's financials or assess acquisition risk.

That gap matters more than ever. NALP data for the Class of 2024 counted over 2,600 JD-advantage jobs, nearly half of them in the business sector, spanning banking, finance, and accounting.

Corporate development, compliance, consulting, and private equity are all accessible to JDs. In every one of those paths, fluency in financial statements is a baseline expectation — not a bonus credential.

This article maps the exact course outline any lawyer should follow to get financially literate before stepping into a business career.

Key Takeaways

- Financial statement analysis is foundational for JDs targeting corporate, finance, compliance, or consulting roles

- A structured course covers six core areas — from income statements and cash flow to ratios, red flags, and regulatory frameworks

- Lawyers already have the critical reading and risk-identification instincts — the gap is technical vocabulary, not analytical ability

- Building this skill directly expands the nonlegal roles open to JDs, from transaction advisory to compliance leadership

- Ex Judicata's Financial Fluency for Lawyers course and 100%-nonlegal Job Board give JDs the tools to make that move

What Financial Statement Analysis Is — and Why It Matters for Lawyers

The CFA Institute defines financial analysis as interpreting and evaluating a company's performance and position within its economic environment. In practical terms, it means reviewing three core documents — the income statement, balance sheet, and cash flow statement — and drawing conclusions about a company's health, risk profile, and strategic direction.

For lawyers moving into business roles, this skill shows up constantly:

- Evaluate acquisition targets in corporate development roles by reading audited financials and flagging risk

- Run due diligence in private equity, where earnings quality, cash generation, and balance sheet strength are central

- Identify anomalies in financial disclosures as a compliance or risk function

- Advise clients in consulting by analyzing revenue, expenditure, and employment data

- Interpret financial reports as a nonprofit board member or executive

The good news for JDs: the analytical instincts are already there. Lawyers are trained to read dense, structured documents and flag what's missing, inconsistent, or misleading. Applied to a 10-K, those habits become genuine competitive advantage. The learning curve is technical vocabulary and document structure, not raw analytical capacity.

Course Outline: Six Core Modules in Financial Statement Analysis for Lawyers

Module 1 — The Financial Reporting Ecosystem

Before you can analyze financial statements, you need to understand where they come from and why they're structured the way they are.

This module covers:

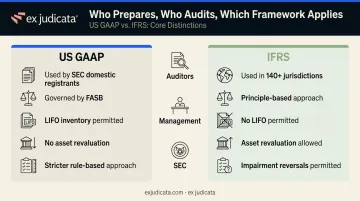

- GAAP vs. IFRS: SEC domestic registrants file under US GAAP; foreign private issuers may use IFRS. Companies in more than 140 jurisdictions are required to use IFRS. These frameworks differ on key issues — inventory valuation, asset revaluation, and impairment reversals — in ways that can materially affect reported numbers

- Who prepares and audits financial statements: management prepares; external auditors attest; the SEC's recognized standard-setter for US public companies is FASB

- How lawyers encounter these documents: due diligence, contract review, litigation, regulatory filings, and business advisory work all surface financial statements in different contexts

This module establishes the vocabulary and context lawyers need before working with the documents themselves.

Module 2 — The Income Statement (Profit & Loss)

The income statement reports revenue and expenses over a period and arrives at net profit or loss. For lawyers learning to read one, the structure is straightforward — the interpretation requires more attention.

Key line items to understand:

- Revenue, cost of goods sold, and gross profit

- Operating expenses and EBITDA

- Net income after taxes and interest

What lawyers should specifically look for:

- Revenue growth trends across multiple periods

- Margin compression (gross margin shrinking even as revenue grows)

- Unusual expense spikes that don't recur

- One-time items disguised as recurring revenue — a pattern the SEC has pursued aggressively, including a case where Pareteum overstated revenue by 91% in early 2019 by recognizing sales before delivery

Module 3 — The Balance Sheet

The balance sheet is a snapshot at a single point in time: assets equal liabilities plus shareholders' equity. That snapshot can reveal as much about risk as months of operational data.

| Category | What to Examine |

|---|---|

| Current assets | Cash, receivables, inventory — signals short-term liquidity |

| Long-term assets | Property, equipment, goodwill — assess recoverability |

| Current liabilities | Near-term obligations — can the company meet them? |

| Long-term debt | Leverage and solvency risk |

| Shareholders' equity | Book value and capital structure |

Key concepts: working capital (current assets minus current liabilities), leverage (how much debt funds operations), and solvency (whether long-term obligations are manageable).

Module 4 — The Cash Flow Statement

Profit and cash are not the same thing — and for lawyers accustomed to document-level analysis, the distinction is often counterintuitive.

Profit and cash are not the same thing — and for lawyers accustomed to document-level analysis, the distinction is often counterintuitive.

The income statement uses accrual accounting: revenue is recognized when earned, not when cash arrives. The cash flow statement tracks actual cash movement across three categories:

- Operating activities: cash generated by core business operations

- Investing activities: capital expenditures, acquisitions, asset sales

- Financing activities: debt issuance, repayment, dividends, equity raises

A business can report a profit while running out of cash. A company with strong operating cash flow but heavy financing outflows may be servicing debt it can't sustain. Reading the cash flow statement alongside the income statement shows whether reported earnings are backed by actual liquidity.

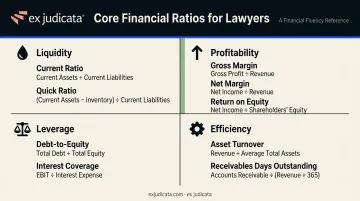

Module 5 — Financial Ratios and KPIs

Ratios convert raw numbers into comparable signals. Used alone, a ratio means little. Compared against prior periods and industry benchmarks — available through resources like Damodaran Online — they tell a clear story.

Core ratios for lawyers to know:

- Liquidity: current ratio (current assets ÷ current liabilities); quick ratio (excludes inventory)

- Profitability: gross margin, net margin, return on equity

- Leverage: debt-to-equity, interest coverage (EBIT ÷ interest payments)

- Efficiency: asset turnover, receivables days outstanding

Knowing what each ratio signals — and when a number should prompt a follow-up question — matters more than memorizing the formulas.

Module 6 — Identifying Red Flags and Conducting Critical Review

This is where lawyer instincts and financial analysis converge most directly. The adversarial reading skills JDs develop in litigation and contract review apply directly here.

Red flags to watch for:

- Net income rising while operating cash flow is flat or declining

- Receivables growing faster than revenue (possible channel stuffing or premature recognition)

- Auditor qualifications, going-concern paragraphs, or adverse opinions

- Frequent restatements — the CAQ analyzed 5,793 restatements from 2013–2022, finding fraud associated with roughly 3% of all restatements and 7% of major ones

- Related-party transactions disclosed only in footnotes

- Accounting policy changes that inflate current-period performance

The Under Armour case illustrates the stakes: the SEC found the company pulled forward $408M in orders across six quarters without adequate disclosure, settling for $9M without requiring restatement. The gap between reported revenue growth and actual demand patterns was visible in the financials — the kind of inconsistency this module teaches lawyers to find and flag.

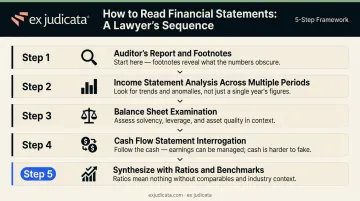

Step-by-Step: How to Read Financial Statements

This is the practical sequence — applicable whether you're preparing for a business role interview, evaluating an acquisition target, or advising a client.

Start with the auditor's report and footnotes. Before touching the numbers, read the auditor's opinion. An unqualified opinion is the baseline; a qualified opinion signals a scope limitation or GAAP departure; a going-concern paragraph changes the entire analytical context. Footnotes reveal what the numbers don't:

- Accounting policy choices

- Contingent liabilities and off-balance-sheet items

- Related-party transactions

Analyze the income statement across multiple periods. Review at least two to three years of revenue and expense lines. Look for margin trends, consistency, and unexplained shifts — and note what the income statement omits: cash timing, asset values, and off-book commitments.

Examine the balance sheet for financial position. Assess liquidity (can it meet near-term obligations?), solvency (is long-term debt manageable?), and asset quality (are assets real and recoverable?). Calculate working capital and leverage ratios directly from the figures.

Interrogate the cash flow statement. Verify that operating cash flow is positive and roughly aligned with net income. Investigate large investing or financing flows — are they funding growth or masking a cash crisis? The gap between reported profit and actual cash generation is where financial fraud most often surfaces.

Synthesize with ratios and benchmarks. Calculate the core ratios from Module 5 and compare against industry norms using sector-specific databases. The final question isn't whether the math works — it's whether the financial story the company is telling holds up under scrutiny.

Applying Financial Statement Analysis in Nonlegal Careers

Consider a former litigator interviewing for a corporate development associate role. The hiring manager asks her to review a target company's financials and flag key risks before an acquisition meeting.

She pulls the auditor's report: qualified opinion, footnote disclosing a contingent liability. She scans three years of income statements — revenue grew 18% last year, but gross margin compressed from 42% to 36%. She checks the cash flow statement; operating cash flow is flat despite the revenue increase.

She calculates the current ratio: 0.9, below the industry average of 1.4. She drafts a two-page summary identifying the margin compression, the liquidity concern, and the contingent liability as the three issues requiring reps and warranties protection.

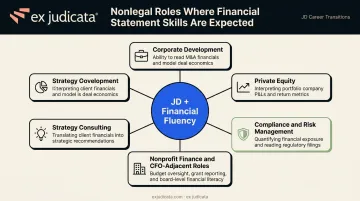

That's the skill set. And it maps directly to roles that actively seek JDs:

- Corporate development — acquisition due diligence and financial risk assessment

- Private equity — earnings quality review and cash-generation analysis

- Compliance and risk management — financial disclosure review and regulatory exposure

- Strategy consulting — financial data analysis and business performance assessment

- Nonprofit finance and CFO-adjacent roles — budget oversight and financial reporting

What distinguishes a lawyer-turned-analyst from a pure finance professional is the ability to translate financial findings into legal and contractual risk language — drafting precise summaries that flag regulatory exposure alongside accounting concerns. Employers in corporate development and private equity actively recruit for it, and few candidates outside the JD pipeline can offer it.

How Ex Judicata Helps Lawyers Build Business-Ready Financial Skills

Ex Judicata was built for lawyers who already think analytically — and need structured training in financial concepts to compete for corporate and business roles.

The platform's Financial Fluency for Lawyers course is taught by Professor Matt Barrett of Notre Dame Law School. His textbook, Accounting for Lawyers, is used in roughly 90% of U.S. law school curricula.

The course covers the balance sheet, income statement, and cash flow statement in a format built for legal professionals — not finance undergraduates. It's designed for attorneys actively moving into corporate and business roles.

Beyond that course, the Ex Judicata platform offers:

- A Job Board with 100% nonlegal roles — corporate development, compliance, consulting, and risk management positions where financial literacy is expected

- The EXJ Career Diagnostic, which maps eight attorney traits to 25 business career paths

- Career Corner coaching from vetted specialists, including professionals with Wall Street and financial services backgrounds

- The EXJ Community, a peer network for non-practicing lawyers already working in business roles

For a lawyer targeting finance, strategy, or corporate development, financial statement fluency is one skill among several. Ex Judicata's platform covers the rest — from the Career Diagnostic that identifies the right target roles to the Job Board and coaching that get you there.

Frequently Asked Questions

What are the topics covered in a financial statement analysis course?

Core topics include income statement analysis, balance sheet review, cash flow statement interpretation, financial ratios, audit reports and footnote disclosures, and red-flag identification. A well-structured course for lawyers also covers the regulatory context — specifically the difference between GAAP and IFRS and how each affects reported numbers.

Do lawyers need to understand financial statements to work in business roles?

Most business-facing roles — corporate development, compliance, consulting, private equity, and risk management — expect at least a working ability to read and interpret financial reports. Depth requirements vary by role, but the baseline expectation holds across nearly all senior business positions.

Can a lawyer without a finance background learn financial statement analysis?

Yes. Lawyers are actually well-positioned to learn this skill quickly. The analytical reasoning, document review habits, and risk-identification instincts JDs develop in practice transfer directly to financial analysis. The main learning curve is technical vocabulary and document structure, not prior finance training.

How long does it take to learn financial statement analysis?

A focused course covering the core modules can be completed in a matter of weeks. Practical fluency typically develops through a combination of structured coursework and hands-on practice with real company reports and SEC filings.

Which nonlegal careers most frequently require financial statement analysis skills?

Corporate development, private equity and venture capital, compliance and risk management, strategy consulting, nonprofit finance leadership, and CFO-adjacent roles all require this skill consistently. Investment banking and transaction advisory work demand it at a deeper level.

What is the difference between GAAP and IFRS, and why does it matter for lawyers?

GAAP (used by US public companies) and IFRS (used in more than 140 jurisdictions) represent different accounting rule sets with meaningful practical differences — particularly around inventory valuation, asset revaluation, and revenue recognition. For lawyers reviewing financials from multinational companies or advising on cross-border transactions, understanding which framework applies is essential to interpreting the numbers correctly.