Introduction

Most lawyers entering nonlegal business roles arrive with sharp analytical instincts—and a gap in financial fluency that surfaces quickly. Ask a consulting candidate to walk through why a company's profits are declining, and the ability to think systematically through revenue and cost drivers separates credible candidates from those who guess.

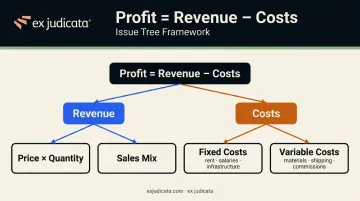

The profitability framework is the structured tool for exactly that: a diagnostic process built on the equation Profit = Revenue – Costs, which consultants, corporate strategists, and operations professionals use to isolate where a business is losing ground—and what to do about it.

This guide is written for lawyers exploring nonlegal careers in consulting, corporate strategy, business development, or adjacent fields. The cognitive work this framework demands is not foreign to legal training—issue spotting, structured reasoning, and hypothesis testing all transfer directly.

What's missing is the vocabulary and the sequence. This guide provides both: a step-by-step breakdown of how to diagnose a profitability problem, the key revenue and cost drivers to examine, and how to apply the framework in a case interview or real business context.

Key Takeaways

- The profitability framework splits every profit problem into two branches: revenue and costs—and lawyers' issue-spotting skills make this structure intuitive to learn

- Revenue analysis covers price, volume, and sales mix; cost analysis separates fixed from variable costs

- Applying the framework without adapting it to the specific business model is the most common mistake lawyers new to this work make

- Numbers reveal where the problem is; qualitative reasoning reveals why—the second step is what makes analysis actionable

What Is the Profitability Framework?

The profitability framework is a structured diagnostic tool that starts with a single equation—Profit = Revenue – Costs—and breaks each side into testable components until the root cause of underperformance becomes clear.

HBS defines the equation as Profit = Total Revenue – Total Costs, where revenue is income from products or services and costs include both fixed items (salaries, rent) and variable items (materials, shipping). From there, the framework expands into an issue tree: Revenue = Price × Quantity, while costs can be segmented by product, customer, geography, or channel to isolate exactly where performance is breaking down.

How It Differs from Audits and Budgets

Professionals sometimes conflate profitability analysis with financial auditing or budget review. They serve different purposes:

| Activity | Purpose | Time Orientation |

|---|---|---|

| Profitability Framework | Diagnose revenue/cost drivers and recommend action | Past variance + forward correction |

| Financial Audit | Test whether statements are free of material misstatement | Historical |

| Budget Review | Estimate income and expenses for a planning period | Forward-looking |

The profitability framework is decision-oriented. It uses the same numbers as financial statements but applies analytical structure and hypothesis testing to reach actionable conclusions, rather than simply documenting historical results.

Why Lawyers Need to Master the Profitability Framework

The Nonlegal Job Market Is Competitive—and Growing

NALP data for the Class of 2024 shows 2,615 JD-advantage positions—roles where a law degree provides a clear edge without requiring bar admission—representing 7.4% of 35,335 jobs taken by that class. Within the business subset, consulting accounted for 11.3% of JD-advantage positions, with compliance at 15.5% and tax at 12%.

These roles exist. But they are competitive, and candidates who cannot demonstrate financial fluency are at a disadvantage from the first interview.

The Skill Gap Is Real Too

GMAC's 2025 Corporate Recruiters Survey—based on 1,108 respondents, including 646 corporate recruiters—ranks problem-solving first and strategic thinking second among skills employers currently value. These are exactly the cognitive skills the profitability framework demands. Candidates who can demonstrate structured, quantitative reasoning in a business context stand out.

Lawyers don't need to become accountants to compete here. They need to close a specific, identifiable gap that shows up in interviews and on the job — and the profitability framework is where that gap is most visible.

Legal Training Is Already Halfway There

Legal issue spotting involves scanning a fact pattern for embedded problems using a trained analytical framework: identifying what's wrong, sequencing the issues, and building toward a conclusion. Consulting issue trees work the same way — decompose the problem branch by branch until the root cause surfaces.

Georgetown Law acknowledges that consultants "use analytical skills gained in legal education to solve problems." The ABA identifies issue spotting as a directly transferable skill to identifying business problems. Lawyers already know how to think this way. What changes is the vocabulary and the data.

Where Ex Judicata Fits

For lawyers ready to close this gap deliberately, Ex Judicata's Financial Fluency for Lawyers course (taught by Professor Matthew J. Barrett, CLE-eligible, $195) is designed specifically for lawyers transitioning to business roles. The platform also connects JDs with vetted career coaches and a job board listing 100% nonlegal roles—including positions in consulting, corporate strategy, and operations where this kind of analytical thinking is a listed job requirement.

How the Profitability Framework Works: A Step-by-Step Breakdown

The framework functions as an issue tree. Start at the top—profit—then move down branch by branch. Structure and sequence matter here, just as they do in a legal memo.

Step 1: Establish Which Side Is the Problem

Before segmenting anything, answer the threshold question: is profit declining because revenue fell, costs rose, or both? Quantify the magnitude of each before going deeper. This prevents spending an hour diagnosing cost inefficiencies when the real problem is a 15% drop in volume.

Step 2: Diagnose the Revenue Side

Revenue breaks into two core components:

- Price — what the company charges per unit, per seat, per transaction

- Quantity — units sold, customers served, or transactions completed

A third factor—sales mix—can erode profit even when total revenue holds steady. If a company shifts toward selling more low-margin products, aggregate revenue can look flat while margins compress significantly.

FTI Consulting's price-volume-mix analysis illustrates why decomposition matters: in one worked example, a $86.6M (20.1%) sales increase was driven by price ($15M), volume ($44.6M), and mix ($27M)—each telling a different story about what was actually driving performance.

Don't stop at whether revenue changed — ask where:

- By product or service line

- By customer type or segment

- By geography or market

- By sales channel

Each segment is a separate hypothesis to test.

Step 3: Diagnose the Cost Side

Once the revenue picture is clear, turn to costs. The fundamental split is between fixed and variable:

- Fixed costs (rent, salaries, infrastructure) don't move with production volume

- Variable costs (materials, shipping, commissions) scale with output

The variable cost formula is: Total Variable Cost = Number of Units × Cost per Unit

This formula matters because it separates two very different problems: a volume problem (selling fewer units) and a unit-cost problem (each unit costs more to produce). Both show up as higher variable costs in aggregate—but they require different solutions.

Step 4: Move From Quantitative to Qualitative

Once the framework surfaces where the problem is—say, unit volume dropped in one product line—the next step is asking why:

- Are customers shifting to a competitor?

- Has the market contracted?

- Is there an internal operational issue driving the change?

- Has regulation changed pricing or cost dynamics?

This is where lawyers have a genuine advantage. Evaluating regulatory shifts, contractual risks, and competitive dynamics is legal work reapplied to a business context.

When structuring recommendations, categorize by impact, feasibility, and timeline. Lead with the conclusion, then support with reasoning — the same discipline legal memos demand, and exactly how consulting deliverables are expected to land.

Where and How Lawyers Can Apply This Framework

The profitability framework isn't consulting-exclusive. It applies anywhere profit matters:

- Management consulting engagements

- Corporate strategy teams

- Nonprofit financial oversight (program costs vs. funding)

- Government budget analysis

- Compliance consulting

- Business development at product or service companies

Customization by Business Model

Applying the framework generically—without adapting it to the business model—is the clearest signal that someone doesn't yet have business fluency. Here's how the variables shift:

| Industry | Revenue Variables | Cost Variables |

|---|---|---|

| SaaS | Subscribers, retention rates | Infrastructure, customer acquisition |

| Healthcare | Payer mix, reimbursement rates, patient volume | Clinical labor, facility overhead |

| Retail | Foot traffic, conversion, average order value | Store labor, occupancy, fulfillment |

McKinsey notes that in retail, replenishment alone can consume up to 70% of store work hours, and e-commerce fulfillment can equal 12–20% of revenue. A lawyer entering retail needs to know those are the cost levers to examine—not a generic fixed/variable split.

What Lawyers Bring That Analysts Don't

Pure financial analysts excel at quantitative decomposition. What they often lack:

- Structured reasoning applied to ambiguous, fact-intensive problems

- The ability to identify qualitative root causes—regulatory shifts, contract exposure, market dynamics

- Clear, persuasive narrative that turns analysis into a recommendation

- Credibility with counterparties who have legal training themselves

The recommendation stage of profitability analysis is fundamentally a writing and reasoning exercise. That's precisely where legal training pays off in a business context.

Those skills translate directly to placement outcomes. Ex Judicata's EXJ Search practice has placed JDs into senior roles at Lockton, Guidepost Solutions, and Marsh McLennan—organizations that specifically seek candidates who combine structured analytical thinking with financial fluency, not as separate hires but in the same person.

Common Mistakes When Using the Profitability Framework

Assuming "Cut Costs" Is Always the Answer

Reflexive cost-cutting is the most common mistake lawyers make when applying the profitability framework. HBR notes that treating cost reduction as a one-off exercise focused solely on short-term savings is myopic—the better framing treats each expense line as an investment whose adjustment shapes future performance.

Bain's PillCo case is instructive: the company didn't cut R&D broadly—it reduced projects 30% while reinvesting 21% of the R&D budget into priority areas, cutting time to market by 28%. That's targeted cost reallocation, not across-the-board cuts.

Revenue-side fixes—pricing adjustments, volume growth, mix optimization—are often more sustainable than cost reduction alone.

Staying at the Aggregate Level

Many first-time users look at total revenue or total costs and stop there. That misses the actual driver. A company can have flat total revenue while losing significant margin because its product mix has shifted toward lower-margin offerings. That dynamic is invisible until you segment.

Confusing Profit with Profitability

Segmentation also clarifies a second distinction that trips up many analysts: profit and profitability are not the same thing.

- Profit = Revenue – Costs (an absolute dollar figure)

- Profitability = a ratio, such as gross margin or operating margin, measuring efficiency

HBS defines gross margin as (Sales – Cost of Goods Sold) / Sales, and operating margin as (Sales – COGS – Other Operating Expenses) / Sales. A company can grow profit in absolute terms while its profitability ratio declines—if costs are rising proportionally faster than revenue. Tracking both gives lawyers a clearer read on whether a client's business is genuinely improving or just growing into a more expensive version of the same problems.

Frequently Asked Questions

Do I need a finance or accounting background to use the profitability framework effectively?

No. The framework runs on basic arithmetic, not advanced accounting. Lawyers who can read an income statement and reason through a problem already have the foundation — and courses like Ex Judicata's Financial Fluency for Lawyers fill in whatever gaps remain.

How is the profitability framework different from reading a company's financial statements?

Financial statements record what happened. The profitability framework is a diagnostic process for understanding why it happened and what to do about it. The framework uses the same numbers but applies structured hypothesis-testing to reach actionable conclusions rather than just documenting outcomes.

Can lawyers apply the profitability framework outside of consulting firms?

Yes. The framework applies anywhere profit matters — corporate strategy teams, nonprofit management, government budget analysis, business development, and compliance consulting all require this kind of thinking. The skill travels well across industries and roles.

What's the difference between revenue and profitability?

Revenue is the total money a business brings in before costs are subtracted. Profitability is a ratio—like gross or operating margin—measuring how efficiently revenue converts to profit. A company can grow revenue while profitability shrinks if costs rise faster, which is why both metrics matter.

Is legal issue spotting similar to using an issue tree in profitability analysis?

Yes, and the parallel is direct. Legal issue spotting means systematically identifying problems within a fact pattern using a trained framework — exactly how consultants build issue trees to decompose profit problems branch by branch. Lawyers tend to adapt to this structure faster than candidates from most other backgrounds.

How do I know whether to focus on revenue or costs first?

Quantify both sides first and compare the magnitude of change. Whichever shows the larger absolute shift is the better starting point. If no data is available yet, revenue problems are more common in practice and usually the stronger initial hypothesis to test.